")

The 3 Components of Infinite Banking Policy Design: Base, PUAs, and Term

Bruce Wehner discusses the primary components of infinite banking policy design: base premium, paid-up additions riders, and term riders. Following the principles laid out by Nelson Nash in Becoming Your Own Banker, we review the concepts for designing a whole life insurance policy for the Infinite Banking Concept.

When Bruce’s father took out a whole life insurance policy on him as a newborn, little did he know that it would be the cornerstone of Bruce’s financial planning in the future.

From leveraging that policy for a home down payment to understanding the value of banking, I’ve followed the policy design guidelines of the Nelson Nash Institute to navigate the complex world of finance.

Join us in our exploration of whole life insurance and the myriad of benefits it offers not just from a security standpoint, but also as a tool for capital growth and liquidity.

In this episode, we touch upon:

- The long-term thinking involved in whole life insurance policy design.

- The three building blocks that make up a solid policy for IBC – and how to mix them just right for your situation

- The nitty-gritty of policy design, discussing why a convertible term policy can be a boon for your financial portfolio.

- We illuminate the often misunderstood relationship between banking and insurance that most financial advisors never talk about

- We examine the financial intricacies of policy design, emphasizing the importance of understanding the connection between a policy’s base death benefit and premium.

- We share insights into how dividends are calculated and how factors such as a low-interest-rate environment can impact these projections.

- Wrapping up, we stress on the importance of affording the premiums and how it affects the potential dividends one can receive.

So, tune in, and let’s debunk the myths surrounding whole life insurance policy design while learning how to make the most of it.

Podcast: Play in new window | Download (Duration: 1:01:02 — 69.8MB)

Subscribe: Apple Podcasts | Spotify | Android | Pandora | Youtube Music | RSS | More

Table of Contents

Whole Life Insurance is Not an Investment

Whole life insurance is a unique place to store cash because it’s safe and it grows. This growth, however, cannot be compared to investments because it’s not an investment. Instead, it should be compared to a bank, which is meant to be “safe” growth. This comparison reveals that cash value in a policy grows at a more substantial rate and is also tax-advantaged.

Cash value is also fairly liquid, though it takes some time for your cash value to catch up to the contributions you make. In other words, there are some limitations on the liquidity early on.

However, this is temporary and is more than worth the trade-off of safe growth — safe from the IRS, creditors, taxation, loss, theft, and death. It’s an iron-clad way to store your cash that you can’t get anywhere else.

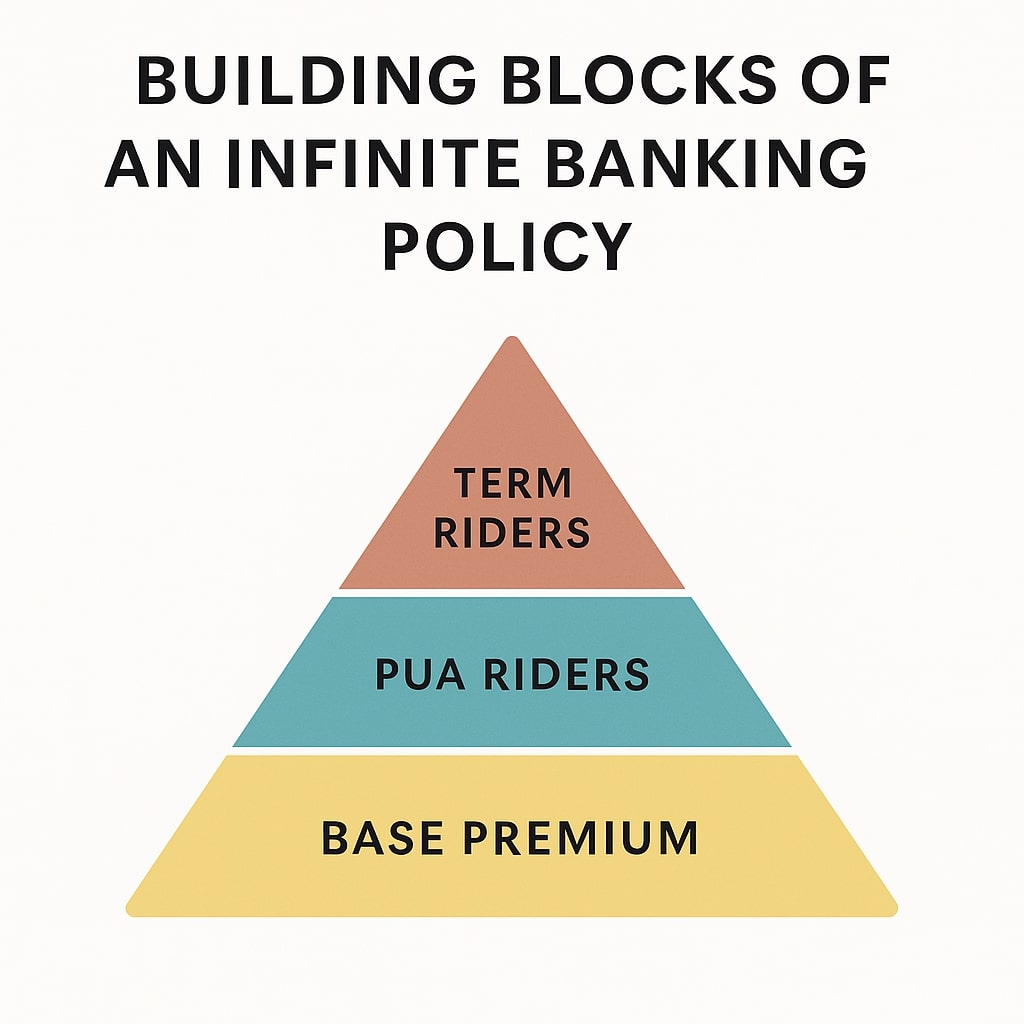

The 3 Components of Infinite Banking Policy Design

In order to get the best results from your whole life insurance policy, you want one that is specifically designed for IBC. This means that you want to work with an insurance agent who is familiar with your financial objectives and can help you choose the ideal policy design.

Policy design can be complex, yet the three main components of a policy are base premium, PUA riders, and term riders.

What is Base?

Base refers to the part of your premium that goes to the main (or base) portion of the death benefit you’re buying. This is the foundation you build the rest of your policy upon, such as PUAs and riders.

When you have a high base, you’re buying more death benefit upfront and paying for it over the course of your premiums.

This means you’ll have slower cash value growth in the beginning because you’re paying over time, and therefore, there are more costs upfront for the company to consider.

After all, the risk is higher to them in the beginning when you’ve only paid a few premiums because they have to pay a death benefit no matter what. Even if you’ve only paid a single premium.

What are PUAs?

PUA stands for paid-up addition, and when you add PUAs to your policy, you’re buying small increments of fully paid-up death benefit. This can accelerate your early cash value growth because you’re buying a small amount of death benefit in one go.

All the cost is accounted for, and it’s low risk to the company since it’s paid-up, so more of it contributes to cash value. It also has the benefit of increasing your death benefit slightly.

Infinite Banking Policy Design and Base/PUA Split

You might hear advisors talking about different “splits,” like a 40/60, for example. This means the composition of your premium is 40% base and 60% PUA. If you’re prioritizing death benefit, you might desire a higher base. If you’re prioritizing early cash value (liquidity), you might desire a higher PUA.

Infinite Banking Policy Example

In the podcast, the example we share is of a $100,000 premium. $40,000 of the premium is going to the base and buys a little over $663,000 of death benefit.

There’s a $2,000 (and change) term rider, which buys an additional $575,000 of temporary death benefit for a 20-year term. And then finally, there’s a little over $57,000 of PUA. This is about a 40/60 split.

This infinite banking policy example illustrates how well-structured policies can provide powerful short- and long-term benefits: access to capital now, uninterrupted compound growth, and a growing death benefit for legacy.

Many people often choose to have several policies over their lifetime, some with the purpose of increasing the death benefit, and some with the purpose of capitalizing.

Ultimately, what you choose now will depend on your goals. And if your goals change, you can always buy additional insurance. You’ll likely want to, as your income increases.

[14:30] “I tell people all the time: Do not overthink this.”

The Role of Term Insurance

If the cost of the term insurance seems high to you, that’s because it is. The reason it’s higher within the policy is because it’s convertible term insurance. This means that the policyholder can convert that temporary insurance into whole life insurance over the course of the contract.

He can do this all at once, a little at a time, or even a partial conversion. And the benefit is that he never has to re-qualify for this insurance. So if his health takes a turn at any point, and he can no longer purchase a brand new policy, he still has the option to convert that term insurance while it’s active.

Adding term insurance can be an invaluable piece of policy design for this reason, especially if you want to maximize your death benefit, and can only afford so much premium. This enables him to get more coverage from day one, with the option to convert as his income increases, too.

The Balance of Infinite Banking Policy Design

There are many components Infinite Banking policy design, and yet ultimately, there’s balance in whatever you choose.

[31:18] “When you pull one lever in an actuarial insurance product, another lever moves.”

In other words, everything you do is a trade-off. When you increase the risk, there’s a trade-off in cost, and vice versa. When you choose to accelerate early cash value, there’s a trade-off in how much death benefit you get.

There’s no option you can choose that’s inherently better or worse, there are just options with different implications.

A common criticism of whole life insurance is that the higher the base premium, the higher the agent commission… so that must be the only reason agents recommend it.

However, if a young family has a need for more guaranteed death benefit, then a higher base is the way to go. Additionally, to balance the lack of early liquidity, the part of your cash value composed of base actually receives a higher dividend. We’ll say it again: Everything is a trade-off, and no option is inherently “bad.”

Liquidity and Thinking Long-Term

The problem many people have with whole life insurance is the lack of early liquidity. When you put in $100,000 the first year, only about $55,000 to $65,000 of that is available to use (with $55k being the guaranteed minimum cash value).

However, if you can be patient and consider the long-term benefits of saving and paying premiums, it pays off.

What you’ll see is that in year 5 of this policyholder’s contract, he pays his $100k premium, while his cash value is projected to increase by $103k. So in only 5 years, his policy is increasing by more than he’s contributing each year.

That said, at this point, he hasn’t broken even. In year 5, his total cash value is $446k and he’s contributed $500k total. Yet, in year 9 his cash value hits that glorious break-even number.

He’ll have contributed $900k, while his total cash value is $920k. From this point on, his cash value will always be more than what he’s contributed (barring a withdrawal). With patience and a mind for long-term strategies, you’ll see the payoff.

Other Facets of Infinite Banking Policy Design

Another responsibility of the advisor is to design a policy you can afford. At a minimum, it’s important to ensure that you can pay the base premium, especially in lean years. PUAs, after all, are optional.

Even so, it’s also critical for an advisor to design a policy with affordable PUAs, too. This is because if you don’t pay them in a given year, you often can’t “catch up.” While realistically, this happens, you also shouldn’t have a policy where you consistently can’t pay the PUAs.

Both the advisor and the insurance company alike should make sure that the policy won’t become a MEC. MEC stands for modified endowment contract, and this is when your contract is no longer considered insurance by the IRS. Instead, they regard it as an investment.

A policy becomes a MEC if you overfund it (based on IRS stipulations), and loses its tax benefits. In other words, it becomes taxable, and you can no longer access the money on a tax-free basis.

👉 Want to learn more about the tax benefits of IBC? Read our article: Is Infinite Banking tax-free.

Generally, insurance companies are diligent about catching if/when a policy is at risk of being over-funded and becoming a MEC. When they do catch this, they help you to rectify the situation.

However, when considering Infinite Banking policy design, it’s the agent’s duty to design a policy with the MEC guidelines in mind, in order to prevent this.

Becoming Your Own Banker: The Power of Purposeful Policy Design

When Bruce’s father placed that first whole life policy in his hands years later, he finally understood what his father had gifted him—not just insurance, but financial sovereignty. This is the essence of what Nelson Nash discovered and what we’ve explored throughout this article.

The magic of Infinite Banking isn’t in complex financial wizardry—it’s in the deliberate orchestration of three simple components of a whole life insurance policy: base premium, PUAs, and term riders.

As you experience the transformation of becoming your own banker, you’ll likely want to add more policies as your goals evolve.

This isn’t just about optimizing a financial product—it’s about reclaiming control of your capital from institutions that profit from your money. It’s about building a legacy that transcends generations, just as Bruce’s father did for him.

So take that first step. Book a strategy call. Start small if you must, but start.

Frequently Asked Questions About Infinite Banking Policy Design

How long until my cash value exceeds my total premiums paid?

This varies by policy design, but typically occurs around years 7-10 for well-designed IBC policies. The example in this article showed a break-even point in year 9, with $920,000 in cash value after $900,000 in total contributions.

Is an IBC policy only for wealthy individuals?

No. While the whole life policy example used for Infinite Banking in this article used $100,000 annual premiums, policies for IBC can be designed for much smaller premium amounts. Many successful IBC practitioners started with modest policies and added more as their income grew.

Can I add more money to my policy later?

Yes! Some people fund their policy at less than the maximum level in some years, and then catch up on premium payments as income increases (limits on how far back you can catch up, and not all companies/products allow this). Others choose to open multiple policies over time to suit new financial goals.

Book A Strategy Call

Do you want to coordinate your finances so that everything works together to improve your life today, accelerate time and money freedom, and leave the greatest legacy? We can help!

Book an Introductory Call with our team today to learn how Privatized Banking, alternative investments, or cash flow strategies can help you accomplish your goals better and faster.

That being said, if you want to find out more about how Privatized Banking gives you the most safety, liquidity, and growth… plus boosts your investment returns, and guarantees a legacy, go to our free guide to Privatized Banking.

You’ll find all your unanswered questions answered there.

What Is a Straight Life Policy? The Simple Answer to a Confusing Term

A straight life policy is simply the base of a whole life insurance contract: a level premium that never changes, a guaranteed death benefit, and guaranteed cash value. If you’ve been researching Infinite Banking, it’s the same permanent insurance you’ve already been learning about, just under an older name. People run into “straight life” or…

Whole Life Insurance Dividend Rates Explained: What the Number Means – and What It Doesn’t

If you’ve researched whole life insurance for Infinite Banking, you’ve probably seen whole life insurance dividend rates advertised. 5.76%. 6.5%. And you’ve probably wondered: is higher better, and how do I compare policies using this number? Here’s the answer, stated plainly: a higher dividend rate does not mean a better policy. Chasing it, without understanding…