")

The Rockefeller Strategy: How Millionaires Use Life Insurance to Build and Keep Wealth

The standard understanding of life insurance goes like this: you buy a policy, pay the premiums, file it away, and hope it never gets used. Protection for your family if you die. That’s it.

But that’s not what wealthy families are doing.

American dynasties, high-profile entrepreneurs, and the country’s biggest banks have been using life insurance as an active wealth-building tool for generations. Not as a replacement for investing. Alongside it. Valued specifically for what it gives them that a brokerage account never can: liquidity, access to capital, and control.

What follows unpacks the actual mechanics and why none of it is reserved for people with a Rockefeller-sized net worth.

Table of Contents

The core ideas:

- Wealthy families treat life insurance as a managed asset, not a forgotten product

- The Rockefeller blueprint combines trusts and whole life to create a cascading, multi-generational capital system

- Banks hold roughly $250 billion in life insurance for the same reasons: liquidity and stability

- Walt Disney, Ray Kroc, and others borrowed against policy cash value to fund businesses banks wouldn’t touch

- Dr. Wade Pfau’s research shows that whole life as a volatility buffer outperforms the “just invest the premium” alternative

- A family bank isn’t a metaphor. It’s a functioning system anyone can build.

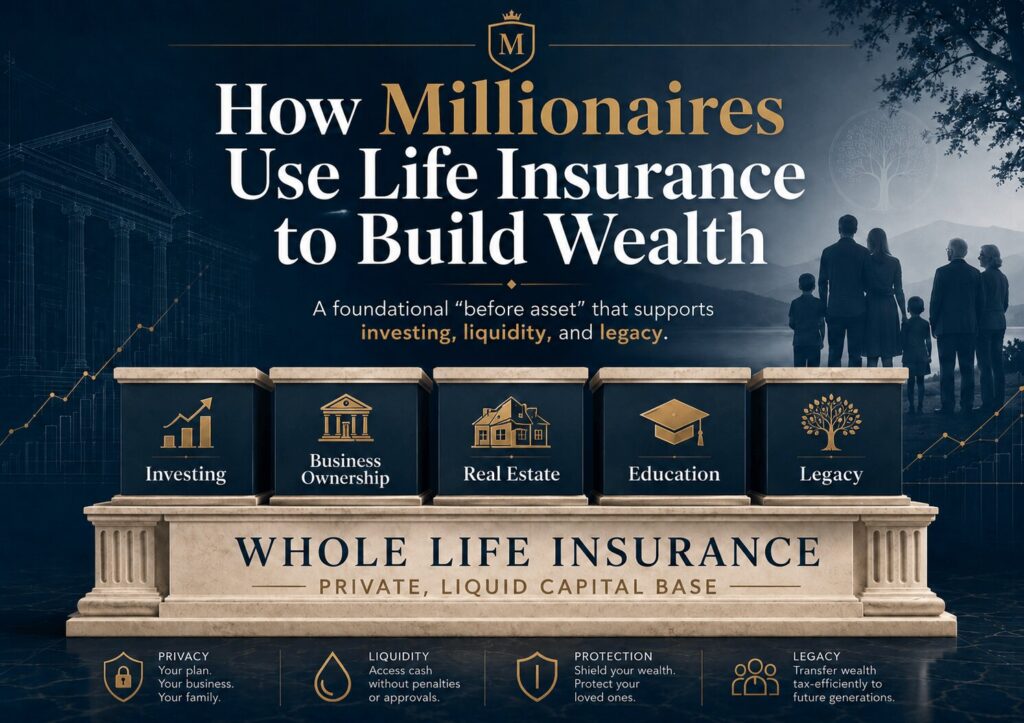

How do the wealthy use life insurance?

Wealthy families use whole life insurance as the foundational “before asset” — a private, liquid capital base that comes before investing and supports every other financial move. They value it for tax-advantaged cash value growth, accessible liquidity that isn’t tied to market cycles, asset protection from creditors in most states, and above all, control over their capital.

Through a combination of policy loans and trusts, they fund businesses, protect assets across generations, and create a cascading system in which each death benefit replenishes the capital pool for the next generation. The same mechanics are available at any level of wealth with a properly designed policy.

How the Wealthy Use Life Insurance Differently Than Everyone Else

Wealthy families could absorb financial mistakes more easily than almost anyone. A bad investment, a failed business, a lawsuit. They’d survive. Yet they still put guardrails in place, specifically through whole life insurance.

If the people who can most afford mistakes still protect themselves this way, what does that say for everyone else? For someone for whom a serious financial mistake isn’t just painful but potentially devastating, the case is even stronger.

The mindset shift is this: wealthy families don’t see a life insurance policy as a product they bought and filed away. They see it as an asset they manage and deploy. The attributes they value aren’t what most people focus on.

They care about accessible liquidity that isn’t tied to market cycles, so a bad year in equities doesn’t force their hand. They care about asset protection from creditors and lawsuits, which whole life provides in most states (not all). And above everything: privacy, flexibility, and access to capital.

Life insurance is private. The only way to know someone owns a policy is if they tell you. That’s part of why this strategy stays largely out of view.

Some of the U.S. presidents who have publicly disclosed their assets have shown whole life among them. That’s notable, not because presidents are financial geniuses, but because they’re disclosing what they actually have.

The wealthy don’t open with “what return does this get?” They open with control, access, and certainty. That order of questions matters.

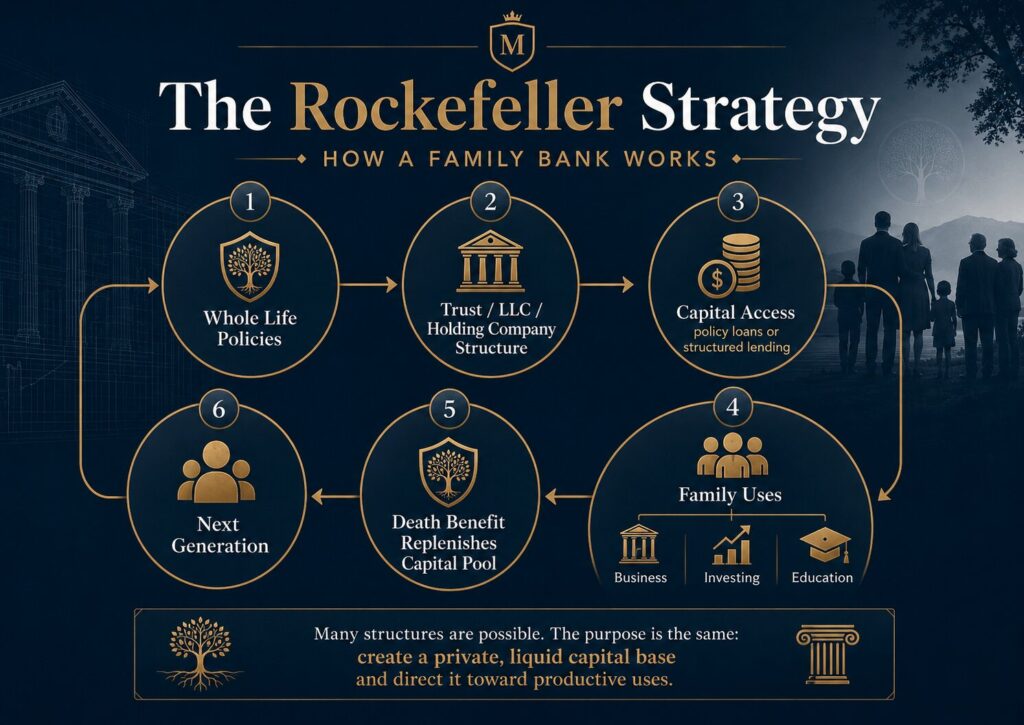

The Rockefeller Blueprint: Trusts, Policy Loans, and the Cascading Death Benefit

The Rockefeller name comes up constantly in Infinite Banking conversations. Almost nobody explains what they’re actually doing.

The Trust and Insurance Combination

Here’s the mechanism. The Rockefeller family combines legal structure and whole life insurance. A family bank can be structured in many ways, depending on the family’s goals, need for asset protection, and desired level of complexity. It may be as simple as outright policy ownership, or it may involve a trust, an LLC, a holding company, or a layered structure where a trust owns a holding company that owns an LLC designed to manage family capital.

The structure can vary, but the purpose is the same: to create a private, liquid capital base using whole life insurance. That capital can then be accessed and directed toward productive uses, such as buying businesses, investing, funding education, or building assets that strengthen the next generation.

The Cascading Effect

When a family member dies, the death benefit doesn’t just get handed out. It’s held in trust and distributed according to the family’s stated intentions, then refills the capital pool for the next generation, who repeat the same cycle.

This is simultaneously a legacy strategy, a banking strategy, a liquidity strategy, and a values-transfer strategy. The trust and the insurance connected together are what make it continuous. Neither piece alone does what both pieces do together.

One nuance worth flagging: trusts are not income-tax magic. In most cases, a trust does not eliminate income tax; it simply determines who reports and pays it, whether that is the trust, the grantor, or the beneficiaries. What trusts can do well is provide structure, accountability, estate-tax planning when properly designed, and a measure of asset protection depending on the type of trust, state law, and how much control is retained. That is real value, but it is a different kind of value than people sometimes imagine.

This isn’t a strategy reserved for famous dynasties. It works at a personal level too, one generation funding policies for the next, death benefits flowing down to nieces, nephews, grandchildren. Generation One is the hardest. The message isn’t that you need to do this at scale immediately. It’s about thinking long-term and taking small, high-quality steps.

How a Death Benefit Becomes the Next Generation’s Foundation

The generational laddering concept, developed by Nelson Nash, sits at the heart of any family banking formula.

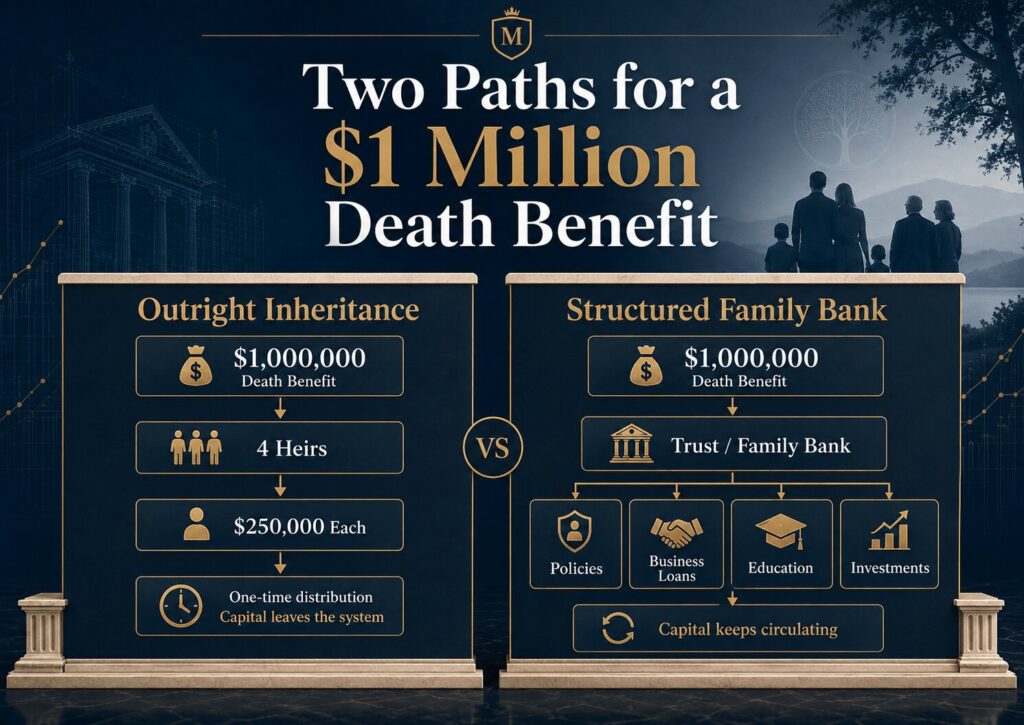

A life insurance policy pays a death benefit. That death benefit funds the premiums on the next generation’s policy. That policy pays its own death benefit, which funds the generation after. You can even skip a generation, grandparents to grandchildren. Each cycle creates a larger pool of capital. It’s a growing family bank, not a one-time inheritance.

The contrast between the two paths is concrete. A $1 million death benefit split four ways gives each child $250,000 outright. No strings. No direction. That’s cutting the cord of accountability. The money is gone from the system. Whatever you hoped they’d do with it is just a hope.

Hold that same death benefit in a trust, with clear intentions that it continues purchasing life insurance, and you have something different. Accountability with guardrails. Clarity and protective measures built into the structure. Not mandating, not controlling from the grave, but providing guidance and continuity.

The goal isn’t to control what your children do. It’s to give wealth a structure that keeps it circulating in the family rather than dissipating in a single generation.

Why Banks Hold Hundreds of Billions in Life Insurance

This is the part many have never heard.

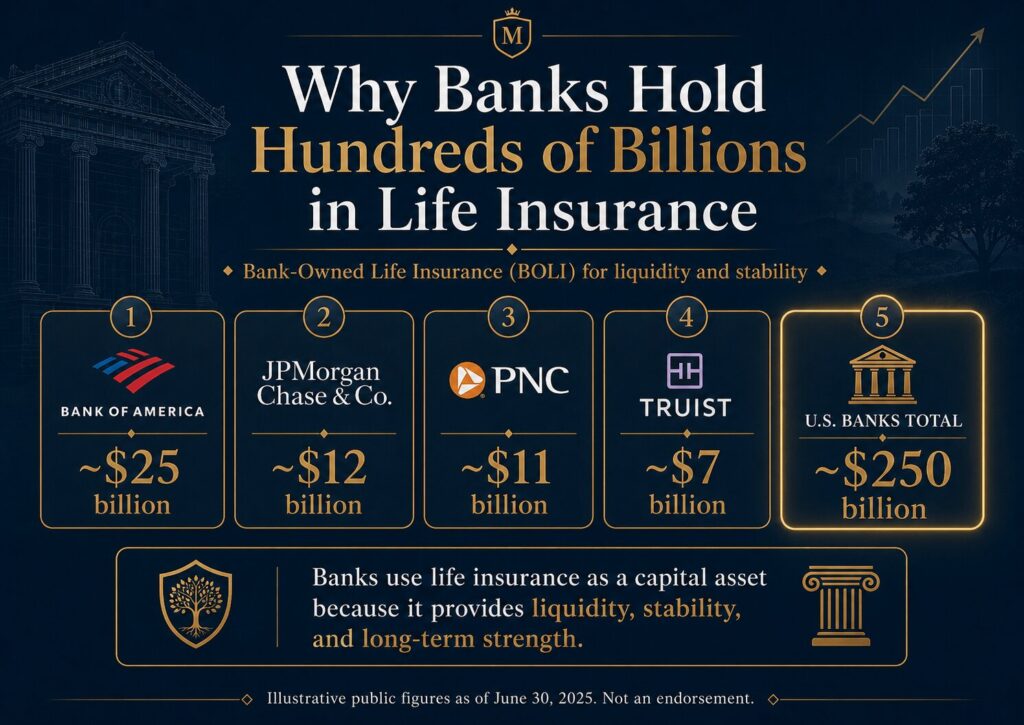

Banks need somewhere to park their Tier 1 capital. Tier 1 capital is the core equity capital that absorbs losses and prevents insolvency. Regulators require banks to hold it and demonstrate they can access it quickly. What banks have consistently chosen as one of those safe places is life insurance.

Bank-Owned Life Insurance, or BOLI, is how it works. Banks take out policies on highly compensated employees and hold the cash value as a capital asset. They use whole life, universal life, and a product designed specifically for banks. As employees age out, they cycle policies onto new people. Regulators cap life insurance at roughly 25% of Tier 1 capital.

The numbers, as of June 30, 2025, are not small:

- Bank of America: ~$25 billion

- JPMorgan Chase: ~$12 billion

- PNC Bank: ~$11 billion

- Truist Bank: ~$7 billion

- U.S. banks total: ~$250 billion

These figures are publicly available via bank rankings at usbanklocations.com, presented here as illustration, not endorsement.

The institutions whose entire job is managing capital and risk at the highest level have parked a quarter-trillion dollars here for liquidity and stability. That’s worth paying attention to. Not because banks are infallible, but because the reason they use it is exactly the same reason the wealthy use it, and the same reason it’s worth considering in a personal financial plan.

How Famous Entrepreneurs Funded Their Dreams With Policy Loans

Walt Disney wanted to build Disneyland, but the banks said no, so he borrowed against his life insurance cash value.

Capital he controlled, on his own timeline, repaid on his own terms. No restrictive bank covenants, no lost equity stake, no waiting for approval. He used it to help build what became a multi-billion-dollar empire.

The key point: he borrowed from his own capital base while the policy kept doing its job. The cash value kept compounding. He didn’t have to sell assets or give up ownership to access what he needed.

Others in the same category: Ray Kroc at McDonald’s; Doris Christopher, who founded Pampered Chef; J.C. Penney; and Foster Farms. These are examples and proof-of-concept, not endorsements of any specific approach.

And it’s not just historically famous names. We’ve helped many clients access cash value to start or expand businesses. The famous names just demonstrate that a strategy ordinary business owners use every day has worked at the highest levels too.

The Volatility Buffer: Using Cash Value to Survive Down Markets

This is where the skeptical reader’s defenses should start coming down.

Dr. Wade Pfau ran 10,000 Monte Carlo simulations on a strategy using whole life cash value as a volatility buffer. A Monte Carlo simulation essentially models thousands of possible market scenarios to see how a strategy holds up across all of them, not just the optimistic ones. And he did this work while at an RIA, a registered investment advisory firm, meaning a money-management company, not an insurance company. That context matters for credibility.

The Problem: Sequence of Return Risk

Market volatility is tolerable while you’re accumulating wealth. It becomes genuinely dangerous once you’re drawing down in retirement.

Here’s why. Say you have $100,000 and the market drops 20%. You’re at $80,000. The next year it recovers 20%. Most people assume they’re back to zero. But 20% of $80,000 is only $16,000, bringing you to $96,000. Not even. And if you’re also pulling out distributions to live on, the hole deepens further each year. A sustained run of this, early in retirement, can be permanently damaging.

The Buffer in Practice

The strategy: in down years, borrow against the policy’s cash value instead of selling investments at a loss. The policy keeps compounding uninterrupted because you’re borrowing against it, not liquidating it. The death benefit later refills the bucket.

Pfau also found that income-producing annuities for a portion of the portfolio can further smooth volatility. Because the life insurance covers the fixed-income role in the portfolio, the investor can afford to be more aggressive with equities. Across 30-, 40-, and 50-year simulations, that investor ends up with more money.

The obvious objection: what if you’d invested the premiums in equities instead? Pfau tested that. Equities still don’t outgrow the strategy, because the damage done in down years is too hard to recover from.

For couples, both holding policies, the surviving spouse doesn’t face the risk of running out. That security gives both partners permission to spend more freely during their lifetimes.

Building a Family Bank: How the Strategy Actually Runs

Banking, stripped to its basics, is storing capital, accessing it, replenishing it, and putting it somewhere safe where it earns without going to zero. It’s the foundation of what people mean when they talk about being your own bank.

Extend that to a family. Make cash value accessible to children, parents, cousins, nieces, and nephews. That’s the start of a family bank. Two phases: cash value during your lifetime, death benefit after it.

Investing in family members means their skills, their business opportunities, their education, and their financial development. Not handing out cash. Investing, with the expectation of a return in the form of growth, repayment, and continuation of the system.

Think of it as foolproof lending. With a contract in place, if a family member borrows and doesn’t repay, the unpaid amount is deducted from their branch of the next generation’s trust share. And if a loan isn’t repaid, or a funded business fails, the death benefit doesn’t just make the loan whole. It grows the trust for the next generation.

The psychology shift matters as much as the mechanics. Thinking in loans rather than outright gifts changes how the recipient shows up. They’re not a passive beneficiary. They’re a co-laborer, a joint steward of family capital. They have to be investable. They’re expected to repay.

That mindset, the understanding that capital is something to steward and circulate rather than spend once, is itself what transfers between generations.

Teach the next generation to take the death benefit, turn it into premium, and repeat the cycle. That’s the family bank in practice.

Why This Strategy Works at Any Level of Wealth

The reason to study what wealthy families do isn’t to admire them. It’s to ask what they know that you can apply.

Billionaires and centimillionaires typically allocate around 5-15% of their net worth to fixed-income assets: bonds, treasuries, and life insurance. The purpose is stability, liquidity, and protection. That logic scales down. You don’t need a Rockefeller-sized balance sheet to build a foundation of controllable, accessible capital that makes everything else in your financial life work better.

Access to capital may be the single most important benefit of the whole strategy. Capital available in good times and bad lets you act when others can’t. We’ve undervalued capital because easy loans and credit cards made it feel abundant. And roughly 16 years of relative prosperity since around 2010 have dulled the memory of why a stable, accessible reserve matters.

The persistent mistake is comparing life insurance based on the rate of return. That’s the wrong question. The real value is what the available capital makes possible, in good conditions and bad.

The first generation is the hardest, especially when inflation is squeezing budgets and costs are escalating. Strategies exist to accelerate how much premium you can put in, to get the system moving faster. But the real payoff is generational.

Imagine being four generations into this rather than starting it. Your great-grandchildren would be in a completely different position.

And it doesn’t tie up money you can’t reach. The advantage shows up during your own lifetime too.

Podcast: Play in new window | Download (Duration: 46:25 — 53.1MB)

Subscribe: Apple Podcasts | Spotify | Android | Pandora | Youtube Music | RSS | More

Model the Successful Few

The wealthy don’t use life insurance instead of investing. They use it as a foundation that makes their investing, their access to capital, and their legacy planning all work better together.

This is not about pulling money out of the market. It’s a liquidity layer that keeps wealth circulating in the family rather than shrinking. Valuing capital and control over chasing return.

You don’t need to inherit generational wealth to begin. You need a properly designed policy and an understanding of how to use it. Success leaves clues, so model the successful few, just like the Rockefellers, and build a life and business you love.

If you want to see how this fits your full financial picture and where to start, book a strategy call with The Money Advantage.

Frequently Asked Questions

Do rich people have life insurance?

Yes, and not just for the death benefit. Wealthy families across generations have used whole life insurance as an active wealth-building tool, valued for its liquidity, tax-advantaged cash value growth, creditor protection in most states, and privacy. Several U.S. presidents who disclosed assets have shown whole life among them.

How do the wealthy use life insurance?

They treat it as a managed asset within a broader financial system, not a product they buy and forget. The primary value they’re after is access to capital that isn’t tied to market cycles, combined with asset protection and the ability to transfer wealth across generations through a combination of trusts and policy structures.

What is the Rockefeller strategy with life insurance?

The Rockefeller family uses life insurance to fund family trusts, which then provide capital to family members through policy loans for business, investment, and education. When a death benefit pays out, it’s held in trust and distributed according to the family’s stated intentions, then refills the capital pool for the next generation. It’s a legacy strategy, a banking strategy, a liquidity strategy, and a values-transfer strategy all at once.

Why do banks own so much life insurance?

Banks need a safe, accessible place to hold Tier 1 capital, the core equity capital that absorbs losses and prevents insolvency. Life insurance provides that. As of June 30, 2025, U.S. banks held roughly $250 billion in life insurance assets, with Bank of America alone holding approximately $25 billion.

Is using life insurance to build wealth instead of investing?

No. This point is non-negotiable. Life insurance is the foundation of an investment strategy, not in place of one. The wealthy use it as a liquidity layer and capital foundation that makes their investing, their access to opportunities, and their family’s financial continuity all work better.

What is the volatility buffer strategy?

Dr. Wade Pfau’s research tested a strategy where retirees borrow against whole life cash value in down market years rather than selling investments at a loss. The policy keeps compounding uninterrupted, the death benefit later refills the capital pool, and across 30-, 40-, and 50-year simulations, investors ended up with more money than those who relied on a standard equity portfolio, even accounting for premiums paid.

What is a family bank, and how does it work?

A family bank is a system where life insurance cash value is made accessible to family members through policy loans, with the death benefit continuing the cycle into the next generation. It’s two phases: access to capital during your lifetime, and the death benefit after. The goal is to keep wealth circulating and growing within the family rather than dissipating with each generation.

Do I have to be wealthy to use this strategy?

No. The mechanics scale. A properly designed whole life policy gives you access to the same liquidity, compounding, and generational transfer principles the Rockefellers use, at whatever level you can start. Generation One is the hardest, but the advantage shows up in your own lifetime, not just for your heirs.

What Is a Straight Life Policy? The Simple Answer to a Confusing Term

A straight life policy is simply the base of a whole life insurance contract: a level premium that never changes, a guaranteed death benefit, and guaranteed cash value. If you’ve been researching Infinite Banking, it’s the same permanent insurance you’ve already been learning about, just under an older name. People run into “straight life” or…

Whole Life Insurance Dividend Rates Explained: What the Number Means – and What It Doesn’t

If you’ve researched whole life insurance for Infinite Banking, you’ve probably seen whole life insurance dividend rates advertised. 5.76%. 6.5%. And you’ve probably wondered: is higher better, and how do I compare policies using this number? Here’s the answer, stated plainly: a higher dividend rate does not mean a better policy. Chasing it, without understanding…