")

Is Velocity Banking the Fastest Way to Pay Off Your House?

Want to pay off your house fast? Considering Velocity Banking? You’re not alone.

So many people are motivated, whether by culture, values, or something else, to pay off their house as quickly as possible.

This desire is completely normal. But it can leave you vulnerable to some pretty big unintended consequences.

When we’re emotionally driven to do something, we can be attracted like moths to a porchlight to anything that promises that thing.

Podcast: Play in new window | Download (Duration: 56:09 — 64.3MB)

Subscribe: Apple Podcasts | Spotify | Android | Pandora | Youtube Music | RSS | More

When it comes to paying your house off fast, one such “porchlight” is Velocity Banking. The widely promoted strategy of velocity banking to pay off a mortgage uses a HELOC to replace your mortgage and pay off your house, usually within 5 – 10 years, and save interest.

The problem is that we can be misled when the messaging hits all of our hot buttons, even if it doesn’t entirely make sense to us.

Save time, save interest? Sounds good, let’s go, right?

Unfortunately, math can be used to tell whatever story you want, depending on what information you skip over or leave out altogether.

When the claims don’t add up, but we’d like them to be true, we reason that someone else already figured it out, so we can just trust them.

Unfortunately,

The lie is easier to tell than the truth is to explain.

Todd Langford

But when something doesn’t add up, it’s time to dig in and ask questions. Your questions are likely more valuable than the answers you find.

When it comes to your money, you deserve real answers so that you can make informed decisions.

That’s why we’re digging into a case study. We’ll answer the question: What is the fastest way to pay off your house?

At its core, Velocity Banking isn’t magic; it’s math combined with leverage and cash flow timing. While the strategy can accelerate mortgage payoff on paper, speed alone doesn’t determine whether an approach is safe or sustainable.

Understanding how the velocity banking strategy actually works helps separate impressive projections from the real-world risks that come with trading predictability for faster payoff.

So, if you want to have the most financial control while paying off your house, tune in now!

Table of contents

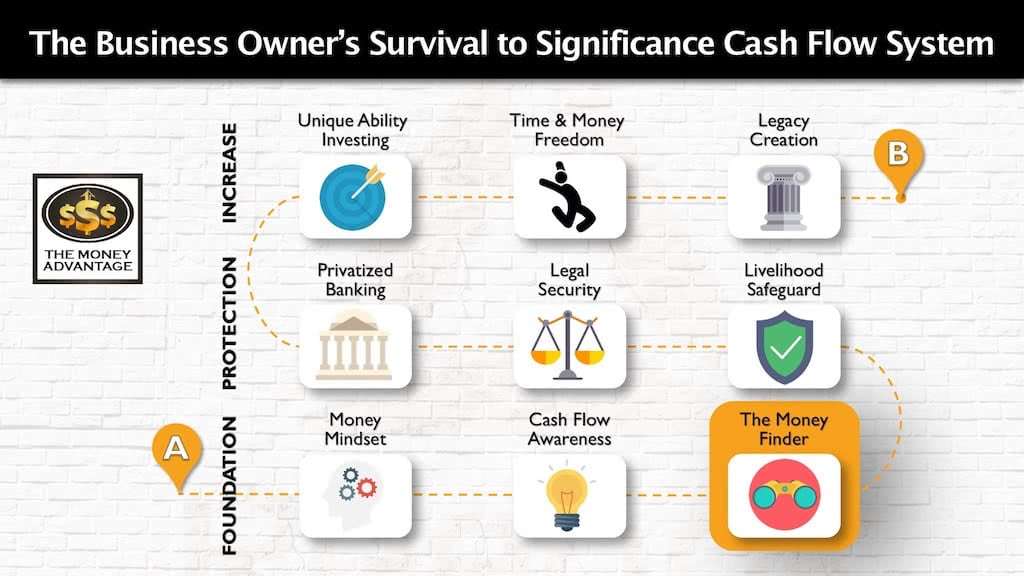

Where Paying Off Your House Fits into the Cash Flow System

Many people looking at velocity banking to pay off a mortgage are missing where this strategy fits (or doesn’t) in the broader Cash Flow System.

Owning a home requires paying for it. And paying for anything, no matter how you do so, affects how much of your money you keep. Making the best financing decisions gives you more to keep and put to work. But no matter how much money you keep, it’s just one small part in the bigger picture of building time and money freedom.

That’s why we have created the 3-step Business Owner’s Cash Flow System, your roadmap to take you from just surviving to a life of significance, purpose, and financial freedom.

The first step is keeping more of what you make by fixing money leaks, becoming more efficient, and profitable. Then, you’ll protect your money with insurance, legal protection, and Privatized Banking. Finally, you’ll put your money to work, increasing your income with cash-flowing assets.

Paying off your house happens right here in The Money Finder step of your financial foundation. When you find, recover, and keep more of the money you’re making, you put more gas into your cash flow machine. However, being debt-free isn’t the same as being in control of your financial future.

What Is Velocity Banking?

At its simplest, velocity banking is a cash-flow management approach that uses a home equity line of credit (HELOC) to accelerate mortgage payoff.

Income is deposited into the HELOC, everyday expenses are paid from it, and surplus cash flow is periodically used to make larger lump-sum payments toward the mortgage. This cycle is repeated to reduce interest costs and shorten the loan term.

Understanding what velocity banking is also requires clarity about what it is not. It isn’t a method for arbitrage interest rates, and it doesn’t eliminate interest through a special banking loophole.

The velocity banking strategy relies on leverage, timing, and disciplined cash-flow behavior, which is why whether velocity banking works depends heavily on stable income, predictable expenses, and rising risk exposure as balances and rates change.

The Case Study

We’ll walk through Truth Concept’s report by Todd Langford and Elizabeth Hagenlocher, Are Accelerated Mortgage Programs Using A Home Equity Line of Credit Effective?

The full report is available for you at the bottom of this article.

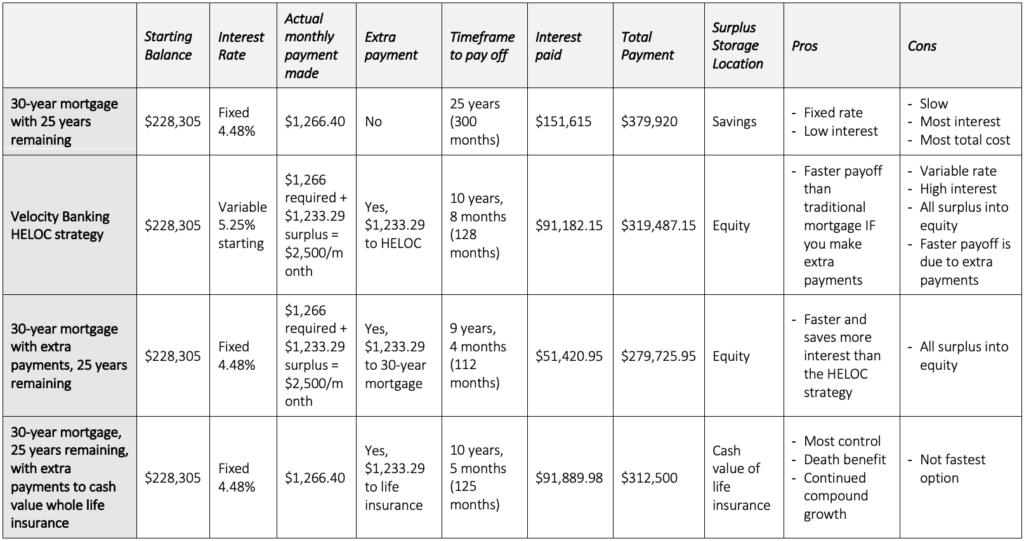

The report analyzes a Velocity Banking example where a person exchanged a 30-year mortgage with 25 years left for a HELOC, paid the house off in 10 years and 8 months, and supposedly saved $217,874.12. This is where velocity banking vs. extra payments becomes a real-world decision.

In the podcast, we compared and contrasted four options:

- Paying the existing 30-year mortgage with minimum payments

- Using a HELOC (Velocity Banking), which included extra payments

- Making extra payments on the existing 30-year mortgage

- Paying the existing 30-year mortgage with minimum payments and storing the monthly surplus in a Privatized Banking system

Here is what we found:

A HELOC Is Riskier Than a Typical Mortgage

The crux of Velocity Banking is that you pay off your house fast by making extra payments. But, rather than making these additional payments on an existing mortgage, you swap out the mortgage for a HELOC.

If you’re comparing Velocity Banking vs. extra payments, it’s important to evaluate the HELOC’s risks and volatility. The stated advantages for using the HELOC over a typical mortgage are that you reduce interest, build equity faster, pay less volume of interest, and can take the money back out if you need it.

A traditional fixed-rate mortgage is a closed-ended loan with known terms: the interest rate, payment schedule, and payoff timeline are established up front. A HELOC, by contrast, is revolving credit with a variable rate and changing required payments over time.

Knowing how this structural shift works is central to evaluating how velocity banking works in practice, and why the added flexibility of a HELOC also introduces uncertainty that doesn’t exist in a standard mortgage.

Risks of the HELOC

Velocity banking depends on a HELOC structure, and HELOCs carry risks that most homeowners underestimate. A HELOC is riskier than a mortgage for these reasons:

- Variable interest rates creating potential open-ended rate increases

- Higher interest rates than mortgages

- Potential increase in required payments

And when it comes to accessing your equity, you may not be able to take your money out, even with an existing HELOC

Variable Interest Rates

With a mortgage, you typically have level, fixed interest rates for the term of the loan. And fixed interest rates mean you have a level payment throughout your mortgage, so it’s easy to plan for that known expense.

With a HELOC, you don’t get that consistency.

That’s because most HELOCs have a variable interest rate that is pegged to the prime rate. And the prime rate is based on the federal funds rate, which can change every six weeks. With a HELOC, you’d always be hoping that rates would stay low, but you’d have no guarantee they’d do so.

Just how variable is the prime rate? The current prime rate as of May 1, 2020, is historically low at 3.25%. But it was as high as 21.5% back in the ‘80s. History shows that you can’t project that the prime will stay unprecedentedly low forever. And if the prime rises while you have a HELOC, your HELOC rates will increase right along with the prime rate.

Higher Interest Rates Than Mortgages

And what kind of rates can you expect with a HELOC?

Generally, expect to pay about 1 – 2% above the prime rate. Today’s HELOC rates are hovering about 4.5 – 5.5%.

Now, you can fix the rate, so you don’t have the unpredictability of rate fluctuations, but you’ll generally pay about another 1%. Today’s interest on fixed-rate HELOCs is about 6 – 6.5%.

All this shows that interest rates are higher on a HELOC than on a fixed-rate mortgage. And the higher rate is where the bank makes its profit.

On two independent Velocity Banking resources, both project rate increases of 0.5% per year. If rates followed that trajectory, in 10 years, interest rates could rise from 5.25% to 10.25% on your HELOC.

Now, will the prime increase, pushing HELOC rates up?

When you’re at historic lows, there’s really only one direction they can go.

But couldn’t HELOC rates decrease as well?

Sure! The point is that you don’t have control when you don’t have a fixed, certain cost, so you’re gambling that everything you can’t control goes in your favor.

Increased Payment Required During the Repayment Period

Another risk of the HELOC is that your required payment increases when you convert from the draw period to the repayment period.

That’s because the HELOC has two distinct chunks of time.

The Draw Period

During the draw period, which is the first 5, 10, or 15 years of the HELOC, you have an interest-only required payment. During this period, you have great flexibility and often a much smaller required monthly payment than on a comparable mortgage.

The Repayment Period

However, once the draw period is over, you enter the HELOC’s repayment period, during which the balance must be paid in full. To accomplish that, the repayment period requires principal and interest.

That means as soon as your draw period is over, your minimum required payment jumps up. In some cases, it could even double.

This transition often catches people off guard because the repayment period feels distant when the strategy is first implemented. Early projections tend to focus on flexibility during the draw period, while the future obligation is treated as a problem that will be solved later.

When required payments increase faster than expected, the strategy shifts from optional acceleration to mandatory obligation, reducing the margin for error if income or expenses change.

Exactly What Will This New Payment Be?

You won’t know for sure until you get there.

The principal amount is fixed to allow for a set pay-off date at the end of the HELOC.

But since the interest rate is variable, the interest portion of the payment can fluctuate. So, the new payment during your repayment window will be based on your outstanding HELOC balance, the duration of the repayment period, and the current interest rate at the start of the repayment period.

Furthermore, because the interest rate is variable, you can have open-ended increases in your required payment that make it very difficult to plan.

For instance, a 30-year HELOC with a 10-year draw period will have a 20-year repayment period. Similarly, a 15-year HELOC with a 10-year draw period will have a 5-year repayment period. A shorter repayment period will require a faster payoff with higher payments.

How Could You Solve This Problem of a Rate Increase?

You could refinance to a new HELOC to begin the draw period over. The only challenge here is that you have to go back through the bank’s requirement process. And that means you’re not guaranteed to qualify for a new HELOC.

This is where many Velocity Banking defenses remain theoretical rather than practical. The idea that you’ll simply adjust to rising rates assumes stable income, uninterrupted access to credit, and continued lender approval, all of which aren’t guaranteed over time.

When evaluating the question “does velocity banking work” beyond spreadsheets and projections, it’s important to recognize that flexibility without certainty shifts risk onto the borrower, especially when rising rates or changing qualifications remove the ability to adapt as planned.

Why Does the Minimum Payment Matter if the Point of Velocity Banking Is to Pay Maximum Payments?

Any time you put a strategy in place, you want to ensure it will work in the best-case scenario when your cash flows, income, and expenses go according to plan, and you have no surprises.

However, you should always ensure that your strategy works in the worst-case scenario, when life gets in the way, such as when income drops or unexpected expenses arise. What if life happens and you can’t make the ‘maximum’ payment?

This reveals the psychological trap of variable obligations: velocity banking strategies often assume you’ll always have extra money available, but real life rarely works that way. The best plans give you the best outcome in the widest range of circumstances.

Velocity Banking vs. Extra Payments: Which Is Truly Faster?

In the report’s scenario, the original house had a $228,305 balance, which was scheduled to be paid off in 25 years, with a 4.48% fixed rate and a monthly payment of $1,266.40.

Here’s how the different strategies compare:

- Velocity Banking (HELOC): 10 years and 8 months

- Extra payments on existing mortgage: 9 years and 4 months

- Standard 30-year mortgage: 25 years remaining

The HELOC strategy paid off the balance in 10 years and 8 months. That’s a faster payoff than the 30-year mortgage, but only if you make extra payments with the surplus of $1,233.29.

If you’d kept the 30-year mortgage and made the same extra payments of $1,233.29, the house would be paid off in 9 years and 4 months. That shaves 16 months off the Velocity Banking strategy, without a new contract, higher interest rate, and riskier terms.

The key advantage of extra payments is that there is no borrowing and no interest rate risk.

This comparison highlights the diminishing returns of leverage within a velocity banking strategy. While introducing a HELOC adds complexity and risk, it doesn’t improve the outcome when the same surplus cash flow is applied directly to the mortgage.

In practical terms, extra payments achieve faster payoff with greater control and fewer moving parts, which is why evaluating the question “does velocity banking work” requires looking beyond speed alone and considering risk exposure and simplicity.

What Is the Safest Way to Pay Off Your House?

Paying off your mortgage should be strategic. Velocity banking may appear faster, but it’s often riskier and less efficient than it seems. But what if you could store the extra payments of $1,233.29 where you had the most control?

If that storage tank was safe from losing value, liquid so you could use it without having to request permission from a gatekeeper, and growing at a substantial rate, couldn’t you build up a balance and then pay off the mortgage in full all at once?

And if you had this cash in your control all along the way, wouldn’t you be in a safer position, since you could get the cash for anything else along the way?

We analyzed a final option of putting the surplus of $1,233.29 into Privatized Banking with a Specially Designed Life Insurance Contract (SDLIC).

If this policy were on a 35-year-old female in average health, you would have sufficient cash value to pay off your house in 10 years and 5 months. At that time, this policy had $163,309 in cash value, adequate to pay off the mortgage balance of $162,504.

We don’t advocate the race to pay off your mortgage at all, because it’s one of the most efficient liabilities you have. The bigger picture objective is financial freedom, not debt freedom. With more cash in your control, you have more options to put that cash to work in income-producing investments.

How to Pay Off Your House Fast and Stay in Control

Bottom line, here’s what we discovered:

- A HELOC is riskier than a typical mortgage.

- The HELOC strategy failed to mention that the early payoff and savings were due to the extra payments and not to the HELOC itself.

- If you paid the same extra payments to the original mortgage you’d pay off your house faster than with Velocity Banking.

- A longer-term loan is better than a shorter term, because of the lower guaranteed required payments that give you more flexibility, cash flow, and control, as you see with a 15 vs. 30 Year Mortgage.

- The safest way to pay off your house fast is to store your surplus cash outside the four walls of your house. Then you can access and use your money along the way. While we don’t recommend paying off your mortgage early, you could do so when you have enough to pay your remaining balance all at once, if that is what you want to do.

You can see our analysis here:

Instead of storing your cash in home equity, we recommend using Privatized Banking with specially designed whole life insurance as your cash storage tank. It gives you the most safety and competitive growth, where you still have guaranteed access to your cash.

The big idea here is that if you want to pay off your house fast, you can do that and still make sure you can use your money along the way for something different if you choose. And having that option puts you in control, with the most safety, choices, and the highest chance of success in the widest range of circumstances.

When viewed through this lens, the priority becomes clear: liquidity comes first, predictability matters more than leverage, and durable systems outperform isolated tactics. Strategies that rely on flexibility, guaranteed access to cash, and long-term structure provide far more control than approaches built around short-term acceleration.

This systems-based mindset is the foundation of The Money Advantage® approach, where decisions are designed to work across a wide range of outcomes rather than only in ideal conditions.

Velocity Banking Isn’t Magic, It’s Leverage

Velocity Banking can work mathematically under the right conditions. When income is stable, expenses are predictable, and interest rates cooperate, the strategy can accelerate mortgage payoff on paper.

But that outcome depends on leverage and assumptions that introduce additional risk rather than removing it.

Whether velocity banking works in the real world comes down to how much uncertainty you’re willing to accept. Replacing a fixed obligation with a revolving line of credit shifts risk onto the homeowner and reduces predictability over time.

Approaching this decision with a clear understanding of trade-offs (rather than speed alone) allows you to evaluate options based on control, flexibility, and long-term resilience.

Find Out More: Build a Smarter Cash Flow Strategy

Get the full report we discussed in this episode here:

Book A Strategy Call

Do you want to learn how to pay off your house without risking your financial stability? Start the conversation today.

We offer two powerful ways to help you create lasting impact:

- Financial Strategy Call – Discover how Privatized Banking, alternative investments, tax-mitigation, and cash flow strategies can accelerate your time and money freedom while improving your life today. Let us show you how to align your financial resources for maximum growth and efficiency. Book a Strategy Call with our team today.

- Legacy Strategy Call – If you want to uncover your family values, mission, and vision, and create a legacy that’s about more than just money, we can guide you through the process of financial stewardship and family leadership. Save time coordinating your family’s finances while building a legacy that lasts for generations. Book a Legacy Strategy Call to learn more about how we can help.

We specialize in working with wealth creators and their families to unlock their potential and build a meaningful, multigenerational legacy.

FAQs

What is velocity banking?

Velocity banking is best understood as a cash-flow strategy that uses a home equity line of credit (HELOC) to accelerate mortgage payoff. Income is routed through the HELOC, expenses are paid from it, and surplus cash is periodically applied to the mortgage balance to reduce interest over time.

Does velocity banking work?

Mathematically, it can reduce payoff time under stable income and predictable expenses. In practice, variable interest rates, changing payment requirements, and reliance on leverage introduce risks that aren’t always accounted for in projections.

Can velocity banking be explained simply?

Yes! Velocity banking relies on timing and leverage, not special interest rate advantages. The strategy attempts to minimize average loan balances by cycling cash flow through revolving credit, which can look effective on paper but shifts risk onto the borrower.

Is velocity banking a strategy or a system?

A velocity banking strategy is a tactic focused on accelerating debt payoff, not a complete financial system. Because it prioritizes speed over liquidity and predictability, it works best when evaluated alongside broader cash flow planning rather than used in isolation.

Short-Term Rentals, with Marilynn Taylor

Is the age of short-term rentals over? If you ask Marilynn Taylor, who coaches investors on successful short-term rental investments, the answer is a resounding no. All it takes is a true understanding of the market and the customer who is seeking a short-term rental. In this insightful conversation with Marilynn, we learn how her…

Real Estate Investing in Today’s Economy, with Anna Kelley

Today, we’re talking with Anna Kelley, impact real estate investor, multifamily operator, and real estate mentor and coach, about the state of real estate investing. With today’s federal debt and high inflation environment, Anna cautions that it’s time to be in capital preservation mode, not focused on cash flow and appreciation. So if you want…