")

Opportunity Cost: The Invisible Cost of Financing

Opportunity cost, like the submerged portion of an iceberg, is a part of your financial decisions hidden from view. While odorless, colorless, tasteless, and silent,

This wealth restrictor is no respecter of persons or purchase types. Opportunity cost is the tag-along to every financial decision you’ll ever make, whether you finance or pay cash. Because a dollar is a seed, every time a dollar leaves your economy, it takes along with it the harvest it had the possibility to create in your lifetime.

The repercussions of every choice to use your money continue to echo throughout the rest of your life and legacy. And just as with icebergs, what’s beneath the surface, is often more important, and much more substantial.

Podcast: Play in new window | Download (Duration: 36:01 — 33.0MB)

Subscribe: Apple Podcasts | Spotify | Android | Pandora | Youtube Music | RSS | More

Table of contents

Earlier in the Series on Debt

Previously, in Why Debt Free Doesn’t Make You Financially Free, we demonstrated clearly what debt is and what it isn’t, and that rushing frantically to pay off loans may be one of the riskiest financial moves you can make.

Then, in The Right Way to Spend Money: Spender, Saver, or Steward? we discovered the limitations of both the Spender and the Saver. We also uncovered the superpowers of the Steward to create wealth through control, access to capital, and uninterrupted compound interest.

The Whole Truth About the Whole Cost of Financing

Now, let’s pull the curtain back to look at the behind-the-scenes cost of financing. We’ll help you discover the truth, the whole truth, and nothing but the truth, in each method of financing. You’ll see why your purchasing method, more than what you purchase, makes the most difference in your control or loss of control.

We’ll answer:

- What are the real, costs of financing over time?

- What are the real, costs of paying cash over time?

- How do I evaluate the entire cost of my financing options to make the best decisions that give me the most control?

Instead of considering only the face value cost and judging the book by its cover, you’ll gain insight into the opportunity cost of any capital outlay, so you can understand what’s inside each purchasing decision. Rather than purchasing big ticket items in a way to avoid something out of fear, you’ll see the path to making empowered decisions that increase your wealth potential. You’ll go from taking mental shortcuts in purchasing that make you lose control, to a system of thinking that puts you in greater control.

Where Opportunity Cost Fits into Your Cash Flow System

Limiting your opportunity cost is just one part of your Survival to Significance Cash Flow System.

The more you reduce the money leaking out of your control today, the smaller your opportunity costs over time. Consequently, the more wealth you have to protect and turn into streams of income.

#1: The Concept of Opportunity Cost

The Cost and Opportunity Cost of Financing

It’s easy to see that when you pay with a loan or credit, you’ll pay interest. That’s the part of the financing decision above the surface, the cost of financing at face value.

But over time, you give up a lot more than the dollars of interest.

The bottom half of the iceberg – the opportunity cost of paying interest – is the echo of that expense. It’s what those monthly payments could have earned for you, had you kept them. In other words, opportunity cost is what you didn’t get. The opportunity cost of financing is what you could have done instead if you didn’t have the payments. It’s what those payments could have grown into, if you’d been able to save and invest them instead.

Easy enough, right?

Why Paying Cash Seems More Sophisticated Than Using a Loan

A loan’s obvious interest payment is the red flag of financing. It warns, “Hey, when you pay interest, you’re paying more than the full cost of the item. It’s costing you more than the face value, and it’s causing you to lose money.”

This is why paying cash seems like a better decision than taking out a loan. The apparent cost is less since you don’t have to add in the interest. Consequently, it seems like you’re keeping more of your money.

But Paying Cash Is Expensive, Too

However, – a really big however – paying cash has a cost and an opportunity cost, too!

The cost of paying cash is the cash itself. The opportunity cost of paying cash is the interest the cash could have earned, had you kept it, that you no longer get to earn because you don’t have the cash.

We humans have a funny way of looking at

This phenomenon is not limited to personal finance, as we observed in our discussion about corporate finance with the concept of Economic Value Added.

The interest you pay when you finance is money you had that’s being taken away. That’s why it’s an apparent loss. What’s harder to see is what your cash could have done for you, had you kept it.

Additionally, the low-interest rate environment saps our creativity. We can’t possibly see how we could earn much on our cash, causing us to have no idea of our true potential. Imagine you could get a higher return on your savings. Would that change the equation for you? What if you knew you could save your cash and earn between 3 – 5% on your money while it was waiting to be used, and then could also invest it at 12% cash-on-cash returns in real estate or businesses? Would that help you see how valuable your cash is? Remember, opportunity seeks liquidity.

The opportunity cost of cash is the part of the financing iceberg that lurks beneath the surface of the water. The submerged part of the iceberg that tragically sunk the Titanic is the same hidden blind spot in most people’s financial decision-making that could sink you too.

You Finance Everything You Buy

I’ll admit, the word financing is a little deceptive because it seems that it means to get a loan.

However, financing simply means “the process of providing funds.”

When you get a loan, you use the funds of another party and pay a premium to do so. The premium for using other people’s money is the interest you pay.

But, when you pay cash, you don’t avoid the premium, it just comes in a different form.

When you pay cash, you self-finance by providing your own funds. To make the purchase, you deplete your cash reserves. The money leaving your control takes along with it the interest it could have earned, had you kept the cash.

All capital, regardless of whether it’s yours, the banks’, or an investors’, has a cost.

This boils down to the Interest Principle.

The Interest Principle: You are always paying interest.

You either pay interest when you finance, or you give up the interest you could have earned when you pay cash.

If There’s a Cost, There’s Always a Corresponding Opportunity Cost

When there’s an iceberg visible above the water, there’s always a corresponding mass of ice beneath the water as well. Likewise, whenever you have a cost, there’s always an opportunity cost.

When you take a loan, you pay interest. The monthly payments are your cost. Your opportunity cost is what the payments could have earned for you over time, had you kept them.

Similarly, when you pay cash, your cost is the cash itself. Your opportunity cost is the interest you could have earned on that cash, had you kept it.

Opportunity Cost over Time

You can best understand opportunity cost if you zoom way out from living in your life and look at the impacts of your decisions over time. Imagine taking off in a jet, high above the timeline of your life, and viewing all of your lifespan in one glimpse.

Your Wealth Potential

If you were to measure all of the dollars that flow into your hands during your lifetime, you’d be astonished by the impressive quantity. For example, a $100K income earned each year, over 40 working years, is a total of $4 Million. This is the income potential.

Your income potential is the sum total of all the money you’ll ever earn. You calculate your income potential by simply adding each year’s income to the next year’s throughout your working career.

Every dollar you earn, if saved or invested, converts from income potential to wealth potential.

On the earning side, you’d be even more astounded if you fully maximize your income by completely developing your potential to create value.

On the investing side, if you put every one of those dollars to its highest use, investing in cash-flowing assets you know and control, you would create surely time and money freedom.

For the ease of understanding, let’s just imagine you invest ALL of those $100,000 every year, for 40 years, and could earn an annual 5% on your money. At the end of 40 years, you’d have over $12 Million! That is the wealth potential in this example.

Now, no one can save and invest every dollar they earn. Much of our money is used up in some way, exiting your personal economy, never to work for you again.

Every Dollar That Exits Your Personal Economy Erodes Your Wealth Potential

If we examine the seed-like potential stored in each dollar that comes through our hands, we realize the jeopardy we place our wealth in when we eat or spend, our seeds.

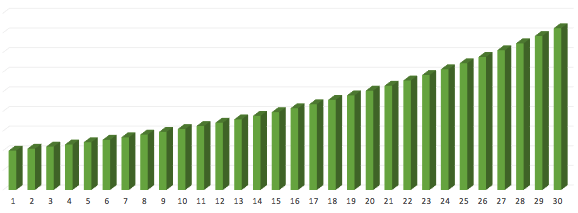

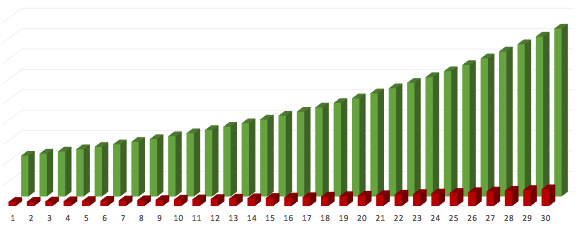

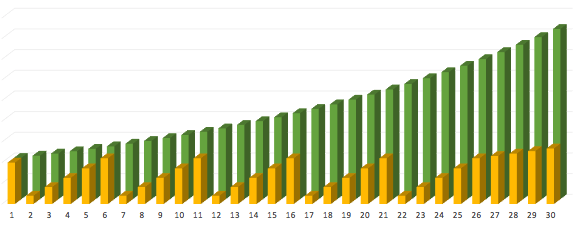

Let’s look at it this way. If you had $100,000, put it to work for 30 years at 5% annual return, compounded monthly, without adding any new money or taking anything out, you’d end up with about $447K (green bars).

Two things that will maximize your wealth potential:

- The more of today’s dollars you put to work, and

- The longer you let them work for you

When you put more money to work for longer, you realize more of your wealth potential. The opposite is also true. The less of your money you put to work, for less time, the less of your wealth potential you realize.

The opportunity cost is what the dollar can no longer produce for you throughout your entire lifespan because it vanished from your personal economy.

If you spent $90K of your original $100K, it can’t work for you, and the future years of growth on that $90K are lost forever. Instead, you invest only $10,000 at 5% over 30 years, ending up with about $45K (red bars). Using your $90K shrank your wealth potential by about 90%, or by $402,000.

In this example, $90,000 is what you spent, but $402,000 is the opportunity cost of using this money. It’s the wealth that you didn’t create.

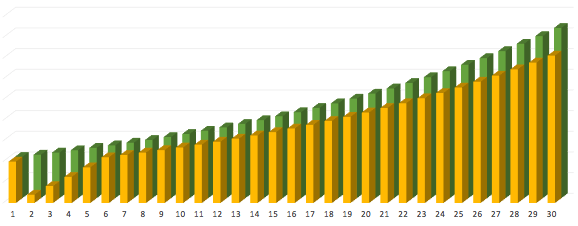

Paying Cash Resets the Compound Interest Curve

Another way to see the opportunity cost of paying cash is to watch the compound interest curve reset every time you use your cash. If you use your $100K just once, even if you put it all back over 5 years, you end up with about $386K. You give up about $61K that money would have created by year 30, just because you pushed back the start of your compounding (see the gold bars with just one dip).

Imagine if you do what so many cash-payers do – stocking their cash account, using it up, and then restocking again – throughout a lifetime! (See the gold bars that dip multiple times.) You never give your money a chance to grow.

Therefore, opportunity cost is the erosion of your wealth potential over the rest of your life, caused by today’s financial decisions.

Comparing the Opportunity Costs of the Saver and the Steward

To bring this idea out of the shadows of the intangible, here’s an example to make it more concrete.

Imagine you had $100,000 of cash and wanted to buy a business that costs $100,000. You’re debating whether to pay cash or use a loan. For illustrative purposes, we’ll assume it’s possible to take a loan for the full amount without a down payment.

How should you pay for it to limit your costs and opportunity costs over time?

Last time, we discussed the three ways to purchase:

- The Spender finances, because they have no cash, and financing with an unsecured loan is their only option.

- The Saver pays cash to avoid paying interest.

- The Steward uses a Private Reserve to keep their cash, financing with a secured loan collateralized by their cash.

For today’s purpose, we’ll compare an example between the Saver and the Steward. We’re taking the Spender’s strategy off the table because in this case, you already have the cash to pay in full. You’re now deciding whether to pay cash and save the interest, or finance and pay interest so you can keep your cash.

That’s really the difference between the Saver and the Steward. Both have cash. They just choose to make the purchase differently.

We’ll look at the measurable impacts, not only right away, but over time.

Ensuring a True Comparison

To make a valid comparison, we must change only one variable. We’ll look at both examples over the same timeframe of 30 years, with equal interest rates in both cases: 5% crediting rate and 5% borrowing rate. Our only difference will be whether we pay cash or finance.

Here, again, you may feel this is unrealistic to earn an interest rate equal to what you’d pay on borrowed money. Low returns on your savings are one of the reasons it’s so hard to envision this concept. For now, persevere in understanding this idea, and then we’ll discuss how to get a higher return on savings and how to think about opportunity cost in spite of uneven interest rates.

Visible Cost

If you take a $100,000 loan at 5% over 30 years, you’d have a monthly payment of $537. Your outflow over the course of the loan will be $193,256, costing you $93,256 of interest over and above the purchase price.

If instead, you pay cash, your outflow will be only $100,000.

Opportunity Cost

Let’s look at the whole costs over time.

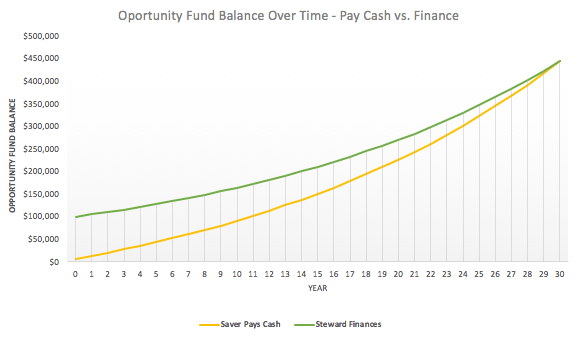

On the one hand, if you pay cash, you give up your $100,000 and what it could have earned for you. Remember, opportunity cost is what you didn’t get. $100,000 earning 5% annually for 30 years, compounded monthly, would have grown to $446,774 by the end of those 30 years. Paying cash causes you to give up $346,774 of interest you won’t create because you used up the cash.

On the other hand, if you finance, you give up cash in the form of a monthly payment of $537 for the next 360 months. Since opportunity cost is what you didn’t get, let’s consider what you could have done with $537 each month if you hadn’t had the payment. If each of those payments had been saved each month and earned 5%, your account could have grown to $446,774 at the end of the 30 years. Financing causes you to give up the ability to save up those payments each month and what they could create.

If you pay cash, your opportunity cost is $446,774. If you finance, your opportunity cost is $446,774. Both options cost you the same! No matter whether you paid cash or financed the $100,000 equipment purchase, the $100,000 decision today cost you $446,774 over the next 30 years!

No matter whether you paid cash or financed the $100,000 equipment purchase, the $100,000 decision today cost you $446,774 over the next 30 years!

I hope it’s apparent that paying cash has a cost, and that saving dollars of interest is the wrong thing to focus on if you want to maximize your wealth creation potential.

Here’s why: if the interest rate you pay and the interest rate you earn are equal, the opportunity cost of paying cash OR financing is equal at the end of the timeframe. Both options deplete your future wealth creation by the same amount.

So, Who Wins?

In this example, it might seem like it doesn’t matter what you do.

However, let’s turn our attention away from what each person didn’t get, and towards their financial status – what they did get – over time.

If you look at the cash position of each person along the way, you’ll notice something interesting.

The person who financed was able to keep their cash. Their cash account started with $100,000 the first year and grew upward to $446,774 in year 30.

The person who paid cash started the first year by immediately dropping their cash account balance down to $0. Over the next 360 months, they added $537/month back to the account, where it earned interest. In year 30, they finish with the same $446,774. It’s important to note that they didn’t just pay into the account the $100,000 principal, but a total of $193,320 of principal and interest.

During all 29 years, 11 months, and 29 days before the 30-year mark, the person who financed had more cash in their account that they could use for emergencies or opportunities. They had a more secure financial footing all along the way.

#3) Determine the Best Financing Decisions

The point is this: all capital has a cost. To be most secure, you want to focus more on what you can earn than on what you pay.

You can reduce your opportunity cost by earning a higher rate on your cash or paying lower rates on financing. Either will increase the spread and give you a greater advantage. Remember that having cash to use as collateral is one of the surest ways to pay lower rates on financing, so it benefits you in both ways.

To earn a higher return on your cash, consider using high cash value whole life insurance. For more information get our free 20-minute guide: Privatized Banking The Unfair Advantage.

Even if you pay a higher interest rate than you can earn, having cash at your disposal gives you control. You’re in a more comfortable, relaxed position to think more clearly, make better decisions, and enjoy life more.

Start Creating Wealth Today

The rest is up to you.

You can continue to undervalue the cost of your capital. You’ll see only the face value of your spending decisions, ignore the opportunity cost, and chisel away at your wealth creation.

Or, you can recognize that all capital has a cost, even your own. With a new respect for the cost of paying cash, you can step into a new paradigm as a Steward and wealth creator. You’ll begin valuing your capital, earning a higher rate of return, and maintaining control.

The Whole Series on Debt

Check out the rest of the articles, podcasts, and videos in the series on debt here:

- Why Debt Free Doesn’t Make You Financially Free

- The Right Way to Spend Money: Spender, Saver, or Steward?

- Opportunity Cost: The Invisible Cost of Financing

- Cash Flow Index: The Smartest Way to Pay off Debt

Build Your Time and Money Freedom

To shrink your behind-the-scenes opportunity costs, and maximize your ability to earn uninterrupted compound interest, consider specially designed whole life insurance as a place to store cash. You’ll earn a guaranteed return much higher than bank rates, as well as highly anticipated dividends, which increase the growth and performance of your cash value. Additionally, you can borrow against your cash value to earn an external rate of return on the same money at the same time, accelerating your wealth.

For more information on Specially Designed Life Insurance Contracts, get our free 20-minute guide: Privatized Banking – The Unfair Advantage.

If you would like to implement life insurance and Privatized Banking in your own life, talk to us about how it would work for you.

Book a strategy call to find out how, and also get the one thing you should be doing today to optimize your personal economy and accelerate time and money freedom.

Success leaves clues. Model the successful few, not the crowd, and build a life and business you love.

Answers to Your Money Questions, Part 3

We’re so thankful for the opportunity to answer your money questions and clear up your confusion. If you’re stuck, we want to help you make sense of the situation so you can move forward. Today, we’re continuing the conversation to answer questions from you—our audience. We want to help you on your quest to control…

Answers to Your Money Questions, Part 2

We all have money questions. If you don’t, you just haven’t asked them yet. Today, we continue to answer questions from you—our audience, tribe, fans, those in a quest to control their money and financial future! You can view part one of this conversation here. There are some great ones here that might be on…