")

Privatized Banking – Life Insurance Loans and Why We Use Them

Life insurance loans are one of the superpowers of the Infinite Banking Concept. They create a powerful financial tool when structured as dividend-paying whole life insurance designed for uninterrupted compound growth. These loans from life insurance policies make the cash value of specially-designed life insurance an ideal pool of capital for your investing strategy. Life insurance policy loans provide the opportunity to earn uninterrupted compound interest and earn a return in two places at the same time.

However, many people encounter

Podcast: Play in new window | Download (Duration: 51:42 — 47.3MB)

Subscribe: Apple Podcasts | Spotify | Android | Pandora | Youtube Music | RSS | More

However, much financial fear is based on partial truth and a lack of understanding of the full range of impacts of your decisions.

And this isn’t your fault. Most “financial education” is a spiffed-up sales pitch offered by “financial experts.” Instead of helping you, it’s a one-way street, viewed through rose-colored glasses, to a particular financial product. Meanwhile, you’re wondering if you will be convinced to buy something you don’t actually want or need.

But, consider this, anything worth understanding has layers of complexity, and only those who pursue a comprehensive understanding will gain it.

This quote by Bryan Bloom strikes at the heart of the matter:

Why isn’t everyone doing this? Everyone who

– Bryan Bloom, Confessions of a CPAunderstands, does.

When it comes to life insurance policy loans, a healthy dose of curiosity will help you gain an understanding of the financial process, principles, and truths that will give you advantages most people only dream of.

Table of contents

What We’ll Cover

In today’s conversation, we’ll answer your questions about life insurance policy loans and why we use them, including:

- What is the function of life insurance cash value in my financial life?

- How does life insurance increase my liquidity?

- What is a life insurance policy loan?

- What can I use a life insurance policy loan for?

- When investing, why would I use a life insurance policy loan instead of paying cash?

- How do I increase my Return on investment by using whole life insurance with my investments?

- Why would I pay interest to “use my own money”?

- Are there times when I should consider another loan with a better interest rate?

- How does a loan from a life insurance policy allow me to grow wealth with uninterrupted compound interest?

Packaging it all together, we’ll demonstrate why they increase returns on your investments.

Where Privatized Banking Fits into Your Cash Flow System

Life insurance policy loans are a part of Privatized Banking, just one step in the greater Cash Flow System.

Wedged between Stage 1 and 3, Privatized Banking fits into Stage 2, the canopy of protection in your financial life. While protecting your personal economy from the risk of loss, it also helps you keep more of the money you make and amplifies your cash-flowing asset strategy, accelerating time and money freedom.

The Function of Life Insurance Cash Value in Your Financial Life

Cash value is part of your savings, a place to store cash. This is your stable, safe money that you save for emergencies and opportunities because it holds its value and provides accessibility.

The function is completely different from your investing. With investments, you’re interested in returns. When you invest, you want to grow your money, either through cash flow or by appreciation.

But life insurance policies are not and will never be an investment. They are a financial tool that when designed properly give you stable access to cash, along with the long-term benefit of uninterrupted compound interest.While your life insurance policy offers growth, its primary benefits are stability of value and ready access.

A Garage to Park Your Money

You could think of putting your money into life policies as parking your cars in the garage.

Driving the cars is where you put them to work, and where all the risk happens.

But no one drives their car 24/7. Between driving excursions, you want a safe, reliable garage to park your car.

The same goes for your money. You need a safe, reliable place to park your capital between investments, where it also gets the most benefits – preferably one that also offers a safe compound interest growth strategy.When planning the trajectory of your financial life, the first question to ask yourself is where you will store your money. The next question is how you will access the money when you need it.

How Life Insurance Increases Your Liquidity

Now that you’re determined to find the best place to store your money between investments, let’s evaluate how a life insurance policy increases liquidity.

One of the major advantages of whole life insurance is that it provides access to liquidity without interrupting growth.To further think this through, here’s a comparison of other savings vehicles you might consider. Note: most other financial products would negatively affect your liquidity and ability to use your money.

Three Parts of a Whole Life Insurance Contract

There are three primary parts of the type of life insurance policy we use:

- Premium Payments

- Death Benefit

- Cash Value

The premium is what you pay into the policy. This is akin to the money you put into savings.

The death benefit is the insurance portion of the contract that is paid to your beneficiaries when you die.

The cash value is the portion of the death benefit you can access during your lifetime. It could be compared to the balance on a savings account. We often call this your emergency and opportunity fund because it’s safe, growing money you can access at any time without interrupting its compound growth.

It is important to note that term life insurance does not provide the cash value needed. You will need a permanent life insurance policy; more specifically, you will want whole life insurance.

The Liquidity of Life Insurance

When you put premium dollars into a specially designed life insurance policy, you can access high cash value right up front—and we’re not talking about a little bit of money. In fact, these policies are structured to give you liquidity early on, with access beginning as soon as the policy is active.

By the first year—typically about 30 days after your payment clears—you can often access 50–70% of your total paid premium. By years five to nine, that figure often surpasses 100%, allowing you to access more than you’ve paid in. From there, the policy continues to grow, earning uninterrupted compound interest through the cash value account.

When you own a permanent life policy, you have a growing pool of capital that you can use.

It’s almost easier to conceptualize what happens when you fund a life insurance policy by thinking of it this way: the money you put in grows, is available to you, and creates a death benefit. In the early years, most of the internal costs are front-loaded, which is why you don’t have access to the full 100% until a few years later.

You have a guaranteed loan provision to access and use your cash value. This allows you to borrow from your policy up to nearly all of its cash value. You can use your insurance policy as collateral to obtain a whole life policy loan from the life insurance company.

And, your cash value is contractually guaranteed to never drop in value, so you’ll never have to worry about losing money.

There are no checkpoints, gates, bars, or denials to accessing your policy’s cash value. The only limitation on how much capital you can get is how much you’ve put into the policy in the first place.

*Individual policies are based on age, gender, and habits. Individual considerations may improve or delay the timeframe of your liquidity.

What Is a Life Insurance Loan?

Let’s take a closer look at what a life insurance policy loan actually is, and why this life insurance loan strategy is a powerful way to access capital without giving up growth potential.

Collateralizing Your Cash Value

When you access your cash value, you are taking a loan from the life insurance company, using your policy as collateral. This method allows you to use the cash value to access loans without interrupting growth.

When you take a loan, the life insurance company places a lien on a portion of your cash value equal to the loan amount. That portion cannot be used as collateral until you start to pay back the loan. As the loan is paid back, the lien is equivalently reduced.

Unlike a credit card or bank loans, there are no requirements. The payback schedule on your loan is entirely up to you. You can pay back as much as you want and when you want.

Rather than decreasing your total cash value, outstanding loans only reduce your available borrowing capacity until paid back.

Total cash value – Current outstanding policy loans = Amount that can be collateralized

Life insurance loans merely reduce the amount that can be collateralized for another loan at the present time. This setup offers a strategic advantage by giving you flexible, ongoing access to capital without forfeiting your asset’s growth.

Here are the implications and benefits to you:

1) You’re Using Other People’s Money (OPM)

You are not borrowing your cash value – you are borrowing against your life policy cash value.

Rather than using your own money, you’re gaining unfettered access to the life insurance company’s capital. Your cash value stays intact, while you deploy other people’s money (OPM) in the ventures of your choosing.

2) You Earn Uninterrupted Compound Interest

Because your own money stays securely intact, at any point in time, with or without loans, your total cash value continues to rise steadily. It does so by earning interest and dividends.

That means you’re earning in two places at once—your policy continues to accrue uninterrupted compound interest, while your borrowed capital generates returns elsewhere.

Because your own money continues to grow, you leverage the power of uninterrupted compounding.

3) You Recycle Your Cash

When you repay the loan, whether incrementally or all at once, you release the cash value to be used again.

This capital access is similar to a HELOC. With a HELOC, current balances are secured against the property’s equity, and repaid balances free up the equity to collateralize another transaction. The difference is that, with a HELOC, the underlying value of the property has the potential to fluctuate and even drop in value, while the underlying cash value in your policy will never go down in value.

This is how cash flow recycling works—you regain access to the same capital over and over again, multiplying its usefulness.

As you continue this process, you create what’s known as ROI stacking: reusing capital for multiple returns without depleting the original source.

Putting the same money to work over and over again is only possible if you maintain control of your capital. You never give up your cash and put it into someone else’s hands. Instead, it remains at your service, able to be collateralized over and over again.

This recycling provides your money with multitasking capabilities and increases its velocity.

Think of it this way. Within equal timeframes, if you could only use your money once, you’d need to get the highest return possible, say 20%. What if instead, you used the same dollars over and over 20 times, earning 10% each time. If every time you sent out the capital to work for you, it brought back a harvest, you would have created a 200% return. This is the power of velocity.

Why “Paying Interest to Use My Own Money” Is a Myth

This statement comes from a slight misunderstanding. With a life insurance loan, you’re not using your own money. Instead, you’re borrowing the life insurance company’s funds. When you use the life insurance company’s money, you pay them interest to use their capital. The interest accrues, adding to the loan balance, if not paid back. Meanwhile, your own money—your cash value—continues to grow, earning uninterrupted compound interest.

The primary objection to using policy loans is usually some form of the question, why would I pay interest to use my own money? But here’s the reality: you’re not withdrawing your funds. You’re using your policy as collateral, which allows your cash value to keep growing while you access capital elsewhere. That’s the key benefit of a life insurance loan strategy—leveraging someone else’s money while your own continues working for you.

Remember the principle:

All capital has a cost.

- Don’t try to look for capital that has no cost, because it does not exist.

- Using your own cash costs what you can no longer earn on that money.

- Using someone else’s requires the payment of interest.

Using your own cash costs what you can no longer earn on that money. Using someone else’s requires the payment of interest. But when you earn in two places—on your investment and within your policy—you offset that cost with a growth advantage most investors never realize.

Life Insurance Policy Loans Allow You to Continue Earning Interest

The value of using policy loans is not that it removes the cost of capital. Instead, it mitigates the cost by allowing you to continue earning interest at the same time. This benefit is known as uninterrupted compound interest, and it’s what sets this strategy apart from using cash directly. It minimizes your overall cost of capital and gives you the upper hand in being the bank.

The advantage is the ability to control capital and use arbitrage to increase your returns. It’s valuable to look at the sum total of the whole picture, not just the cost of the loan.

The Value of Using Life Insurance Loans to Invest, Instead of Just Paying Cash

Another common question that arises when grappling with the idea of using policy loans to invest is this: Should I pay cash or finance when investing? Wouldn’t paying interest to repay the loan reduce my earnings?

The answer requires a further discussion of what happens when you use a policy loan.

Surprisingly, you’ll discover that using a policy loan to fund an investment not only doesn’t cut into your returns, but far to the contrary. Instead, using this loan boosts your investment earnings.

Fundamentally, here’s the difference:

When You Pay Cash, You Trade Returns

While it may seem more straightforward and direct, paying cash has a notable disadvantage. When you use your cash, you can no longer earn a return on that money in the original account.

When you interrupt your money’s compounding, you stop its earning power. You trade its return for the return that you can get in an outside investment.

Therefore, the opportunity cost of using your own cash is all the future money you could have earned in the original account, had you let it continue to earn compound interest.

When You Use a Life Insurance Loan, You Stack Returns

But when you use a life insurance loan, instead of trading one return for another, you get both, stacking the two returns on top of each other. This concept—often referred to as stacking returns—is a powerful way to grow wealth without interruption.

You continue earning the return in the life insurance, PLUS you earn a return in your outside investment. This is how you gain compound growth from loans: your cash value continues to grow, while the borrowed funds generate additional gains elsewhere.

You don’t have to accept the false dichotomy that you must give up one return to get another. This recognition is the key to understanding the power possible to you with Privatized Banking.

Increasing Your Return on Investment by Using Life Insurance Loans

Here’s a closer look at how life insurance loans increase your ROI through stacking your returns. This approach doesn’t just protect your capital—it gives it more jobs to do, increasing your overall return without increasing your risk.

Imagine you started by putting $45K cash aside for 7 years. In the third year, you buy a $100K property that will cash flow $1000/month. Let’s compare using policy loans vs. cash to see how a policy loan increases your returns.

Using a life insurance loan gives you the flexibility to access capital while keeping your original funds intact and growing.We’ll discuss an overview here, but you can get a full explanation in our Privatized Banking Quick and Easy Guide.

Paying Cash to Fund Your Investment

Your first 7 years of deposits of $45,000 each year are made into a bank savings account that earns 1%. Because the savings account is taxable, it’s subject to your 33% tax bracket, reducing your after-tax growth rate to 0.67%.

In year 3, you take $100K of cash out of the account to purchase the investment property.

Since you paid cash, you own the property free and clear, so you collect the full $1K in rent each month. Over the next 30 years, you will receive $360K in cash flow from the property.

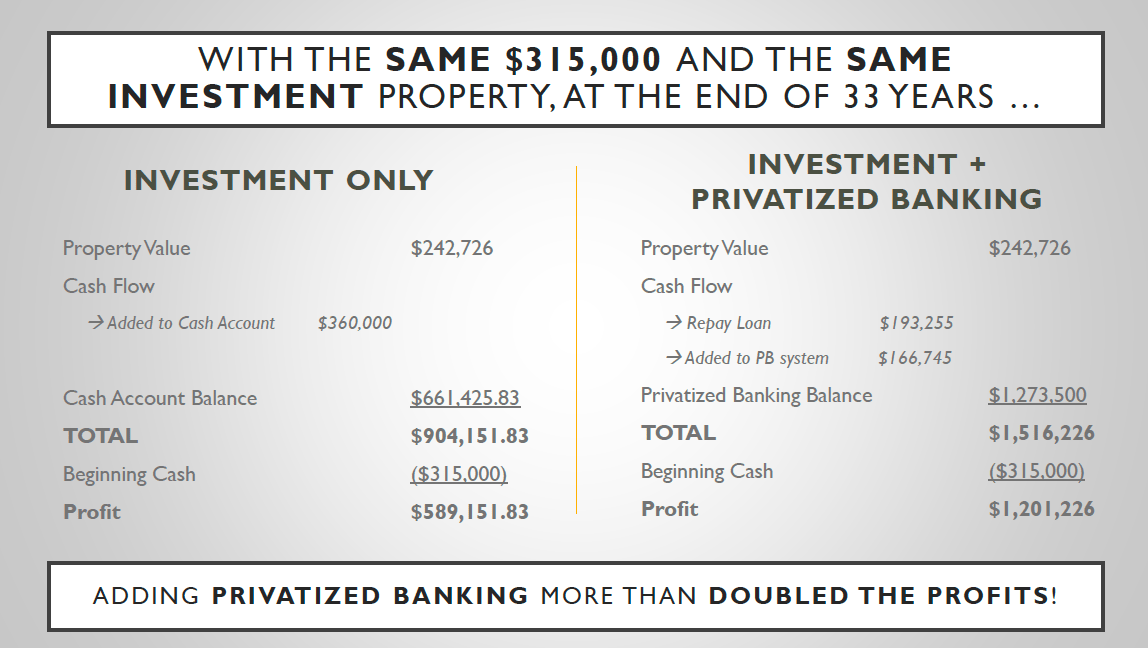

Suppose you deposit the $1K back into the same savings account and leave it there without touching it again. In that case, your ending account balance after another 30 years from the property purchase date (37 years from your initial funding year) will be $661,425.83.

Adding the property value of $242,726, you’d have $904,151,83. We then subtract the $315,000 cash put into your savings account. This leaves you with a profit of $589,151.83.

Private Reserve Strategy with Life Insurance: Using Cash Value to Fund Your Investment

In contrast, instead of placing $45,000 each year into bank savings, imagine you put the same funds into a cash value life insurance policy instead. (An actual life insurance illustration for a 47-year-old man in average health was used for this example.)

Accounting for Loan Repayment

As with the cash-only example, in year 3, you use $100K by borrowing against your cash value with a $100K life insurance loan. Since you are your own banker, you accept the terms of 5% interest. This generates a monthly payment of $536.82, and you’ll pay your loan over 30 years.

Your $1K monthly rental income is reduced by the outstanding loan payment of $536.82/month, leaving you with $463.18/month. This cash flow will be redirected into your Privatized Banking system.

Summing all 30 years of rental payments, less loan payments, you’ll receive a net of $166,745 in cash flow over the next 30 years, after which the loan will be fully repaid.

Yes, this is an amount significantly less than the $360K net cash flow from the property if you paid cash. This is where most people mentally stop with this calculation, but it’s misleading because it doesn’t tell the whole story.

Earning in Two Places at the Same Time

Remember, with the life insurance loan option, you gain returns in two places, not just one. Now we need to look ahead to our policy’s cash value at the end of the measurement period.

Here’s what we find: 30 years after the property was purchased (the 37th year of the policy), the cash value of the life insurance policy, including interest and dividends, amounts to $1,273,500.

Adding the property value of $242,726, you’d have $1,516,226. We then subtract the $315,000 cash put into your Infinite Banking System. This leaves you with a profit of $1,201,226. Compared with the $589,151.83 profit in the cash-only example.

Paying Cash vs. Life Insurance Loans

Using a life insurance policy loan more than doubled the profits at the end of the measurement period. This is because, with life insurance, you earned a higher return in a non-taxable environment, and didn’t reset the compounding on your money. AND you also created a death benefit, a side benefit that wasn’t even considered in the cash-only example.

Therefore, paying interest to use a policy loan doesn’t cut into your earnings. Thinking so stems from viewing just part of the scenario. When you look at the full picture, the end result of this example is that even though you paid interest to access your capital through a loan, you more than doubled your ending balance.

Again, life insurance loans work so well to accelerate your returns because you aren’t trading returns. Instead, you’re stacking returns. You’re earning uninterrupted compound interest in the policy while also earning an external return at the same time.

What Can You Use a Life Insurance Policy Loan For?

If it’s this good, what exactly can you use a life insurance policy loan for? The sky’s the limit here, too!

When you have cash value, you are the only person determining what it will be used for. There’s no approval process, income verification, or paperwork delays – no third party standing over your shoulder to dictate the terms of use.

It can finance the buyout of another business, fund a marketing campaign, or even cover expenses during months of tight income. It can pay for a medical emergency or a new car. You could use it to make a down payment on a house, pay off loans to free up the monthly payments, or buy business equipment.

Obtaining the Best Loan with the Best Interest Rate

Now, just because you have life insurance cash value doesn’t mean you’ll want to use this as your sole capital source.

There are times when you may want to get a bank loan with a better interest rate rather than borrowing against life insurance. In fact, banks will often collateralize a policy’s cash value (not the death benefit) and offer a loan at their going rate for secured loans. This gives you an opportunity to compare and weigh the cost of capital across all available options.

Or, sometimes it makes sense to get a bank loan without collateralizing your policy.

But, if you know your cash can earn 3 – 5% in your policy when your money is at rest, parked in the garage, why would you pay cash and give up the opportunity to earn that return?

The goal is to maintain control over your capital. When you control the money, you can decide which source is best, whether that’s a life insurance loan or a traditional lender. This flexibility brings peace of mind and helps ensure you’re making financially optimal decisions, not just convenient ones.

In Summary

Today, we’ve discussed why you want to use life insurance loans and what they are.

The number one reason to use a policy loan is that it allows you to maintain control of your capital and earn uninterrupted compound interest.

Cash value life insurance is a funding source that provides ready access to capital by offering liquidity through the guaranteed loan provision.

Finally, whole life insurance increases returns on investments by giving you an external return on outside investments, in addition to the internal rate of return that you earn inside the policy.

The strategic use of life insurance loans enables you to access capital without giving up growth, preserve your liquidity, and deploy funds for income-producing opportunities.

Together with the control, guaranteed loan provision, collateralization, uninterrupted compound growth, and the ability to earn returns in two places at the same time, life insurance policy loans give you a multi-dimensional access to capital that you won’t find anywhere else.

Your Decision Point

Now, it’s up to you to decide how to proceed. The only limit on your access to capital through life insurance loans is how much you put in in the first place.

For more information on whole life insurance policies, get our free Quick & Easy Privatized Banking Guide.

If you would like to implement life insurance and Privatized Banking in your own life, talk to us about how it would work for you.

Book a strategy call to get the one thing you should be doing today to optimize your personal economy, accelerate time and money freedom, and start leveraging your cash value today.

FAQs

What is a life insurance policy loan?

A life insurance policy loan lets you access funds by using your cash value as collateral. You’re not withdrawing from your account—you’re borrowing against it. This approach ensures your full balance continues to grow via life insurance uninterrupted compound interest.

What makes a life insurance loan different from a traditional loan?

With a life insurance loan, you avoid the red tape of banks. There’s no credit check or application delay. Your policy becomes your private reserve, giving you liquidity, flexibility, and the benefit of uninterrupted compound interest.

Do I lose growth when I take a loan from my policy?

Not at all (If the insurance company is non-direct recognition). Your entire cash value remains intact and continues to earn life insurance compound interest. You can borrow for opportunities while your capital quietly compounds behind the scenes.

Can I use a life insurance loan for anything I want?

Once you’ve built up cash value, you decide how to use it—whether that’s investing, managing a surprise bill, or making a down payment. That’s the flexibility baked into loan life insurance structures.

Why is compound growth from life insurance loans so powerful?

You earn in two places at once. While your cash value grows with uninterrupted compound interest, your borrowed funds can generate external returns—stacking returns over time.

Whole Life Insurance Dividend Rates Explained: What the Number Means – and What It Doesn’t

If you’ve researched whole life insurance for Infinite Banking, you’ve probably seen whole life insurance dividend rates advertised. 5.76%. 6.5%. And you’ve probably wondered: is higher better, and how do I compare policies using this number? Here’s the answer, stated plainly: a higher dividend rate does not mean a better policy. Chasing it, without understanding…

The Rockefeller Strategy: How Millionaires Use Life Insurance to Build and Keep Wealth

The standard understanding of life insurance goes like this: you buy a policy, pay the premiums, file it away, and hope it never gets used. Protection for your family if you die. That’s it. But that’s not what wealthy families are doing. American dynasties, high-profile entrepreneurs, and the country’s biggest banks have been using life…

2 Comments

Hello:

I have atartwd the insurance process and need financial institutions that fund in the privitized banking area.

Shawn,

Thank you for commenting!

If you are looking for Privatized Banking you can book an appointment here: https://themoneyadvantage.com/calendar